The Balanced Score Card

It was only last night when I was having a heated discussion about how an organisation should fulfill its strategies when I was introduced again to the term 'balanced score card'. I had heard it previously through my workings with AIESEC but hadn't really looked into it in too much depth. Looking into I realised I had implemented many of its elements in my previous projects, but never knew that there was a formalised method as such. Hmmm, Little did I know.

1. Translating the vision into operational goals;

2. Communicate the vision and link it to individual performance;

3. Business planning;

4. Feedback and learning and adjusting the strategy accordingly.

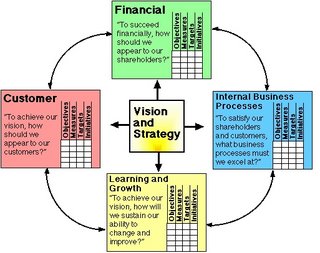

+ Financial perspective - measures reflecting financial performance, for example number of debtors, cash flow or return on investment. The financial performance of an organization is fundamental to its success. Even non-profit organisations must make the books balance. Financial figures suffer from two major drawbacks:

o They are historical. Whilst they tell us what has happened to the organization they may not tell us what is currently happening, or be a good indicator of future performance.

o It is common for the current market value of an organisation to exceed the market value of its assets. Tobin's-q measures the ratio of the value of a company's assets to its market value. The excess value can be thought of as intangible assets. These figures are not measured by normal financial reporting.

+ Customer perspective - measures having a direct impact on customers, for example time taken to process a phone call, results of customer surveys, number of complaints or competitive rankings.

+ Business process perspective - measures reflecting the performance of key business processes, for example the time spent prospecting, number of units that required rework or process cost.

+Learning and growth perspective - measures describing the company's learning curve -- for example, number of employee suggestions or total hours spent on staff training.

The specific measures within each of the perspectives will be chosen to reflect the drivers of the particular business. The method can facilitate the separation of strategic policymaking from the implementation, so that organisational goals can be broken into task oriented objectives which can be managed by front-line staff.

It can also help detect correlation between activities. For example, we might find that the internal business objective of implementing a new telephone system can help the customer objective of reducing response time to telephone calls, leading to increased sales from repeat business.

You can't improve what you can't measure

Balanced scorecard

This is a concept for measuring a company's activities in terms of its vision and strategies. Helping it adhere to its startegic management objectives and gain a clear prescription as to what should be measured in order to 'balance' the financial perspective.- It gives managers a comprehensive view of the performance of a business.

- It is a strategic management system that forces managers to focus on the important performance metrics that drive success.

- It balances a financial perspective with customer, internal process, and learning & growth perspectives.

1. Translating the vision into operational goals;

2. Communicate the vision and link it to individual performance;

3. Business planning;

4. Feedback and learning and adjusting the strategy accordingly.

A Comprehensive view of business performance

The scorecard seeks to measure a business from the following perspectives:+ Financial perspective - measures reflecting financial performance, for example number of debtors, cash flow or return on investment. The financial performance of an organization is fundamental to its success. Even non-profit organisations must make the books balance. Financial figures suffer from two major drawbacks:

o They are historical. Whilst they tell us what has happened to the organization they may not tell us what is currently happening, or be a good indicator of future performance.

o It is common for the current market value of an organisation to exceed the market value of its assets. Tobin's-q measures the ratio of the value of a company's assets to its market value. The excess value can be thought of as intangible assets. These figures are not measured by normal financial reporting.

+ Customer perspective - measures having a direct impact on customers, for example time taken to process a phone call, results of customer surveys, number of complaints or competitive rankings.

+ Business process perspective - measures reflecting the performance of key business processes, for example the time spent prospecting, number of units that required rework or process cost.

+Learning and growth perspective - measures describing the company's learning curve -- for example, number of employee suggestions or total hours spent on staff training.

The specific measures within each of the perspectives will be chosen to reflect the drivers of the particular business. The method can facilitate the separation of strategic policymaking from the implementation, so that organisational goals can be broken into task oriented objectives which can be managed by front-line staff.

It can also help detect correlation between activities. For example, we might find that the internal business objective of implementing a new telephone system can help the customer objective of reducing response time to telephone calls, leading to increased sales from repeat business.

You can't improve what you can't measure

So metrics must be developed based on the priorities of the strategic plan, which provides the key business drivers and criteria for metrics that managers most desire to watch. Processes are then designed to collect information relevant to these metrics and reduce it to numerical form for storage, display, and analysis. Decision makers examine the outcomes of various measured processes and strategies and track the results to guide the company and provide feedback.

So the value of metrics is in their ability to provide a factual basis for defining:

So the value of metrics is in their ability to provide a factual basis for defining:

- Strategic feedback to show the present status of the organisation from many perspectives for decision makers

- Diagnostic feedback into various processes to guide improvements on a continuous basis

- Trends in performance over time as the metrics are tracked

- Feedback around the measurement methods themselves, and which metrics should be tracked

- Quantitative inputs to forecasting methods and models for decision support systems

Some Useful Liks on implementing the BSC

http://www.2gc.co.uk/pdf/2GC-PS050616.pdf

http://www.2gc.co.uk/pdf/2GC-RSS.pdf

http://www.2gc.co.uk/pdf/2GC-SMESME.pdf

http://www.2gc.co.uk/pdf/2GC-BSCEVA.pdf

http://www.2gc.co.uk/forum/viewtopic.php?t=75

posted by the author at 3:20 AM

![]()

0 Comments:

Post a Comment

<< Home